To Convert or Not to Convert…

That is the Question!

Roth conversions are often discussed and, like most things nowadays, every expert seems to have a strong “opinion” and most will argue their opinion is the right one. Which leaves a very confused and bewildered public.

We’re here to help demystify Roth accounts and conversions so that you can become more confident in your personal financial plan.

Key Takeaways

Deferral of taxes and tax savings are very different

We want to defer when taxes are high and convert (pay) when taxes are low

Paying taxes creates an emotional response in most people

Tax planning usually requires action before year-end, not during tax filing season

Conversions, when used strategically, can provide more net spending dollars during retirement

What is a Roth Account?

First off, let’s understand at the highest level what a “Roth account” is.

As part of the Taxpayer Relief Act of 1997, we saw the first legislation that allowed an investor to pay the tax before placing funds into an account that could grow tax-free and ultimately be distributed tax-free after reaching a certain age.

Fun fact: Roth accounts get their name from Senator William Roth of Delaware!

The real power of the account is the ability to “pre-pay” the tax and avoid paying any tax on the investment growth over time. Truly a powerful investment vehicle.

Why Not Put Everything in Roth?

At this point you may say, “Why not put ALL my investments into Roth accounts?”

Well, there are various restrictions and contribution limits that would, in most cases, prevent an investor from doing this. But at a more technical level, it could actually be less tax-efficient over an investor’s lifetime.

Let me first define how I use the term tax efficiency.

The old saying goes, “The only two certainties in life are death and taxes.” But the ability to reduce the overall amount of taxes you pay over your lifetime is effectively a gauge of how efficient your tax planning was.

To be clear, tax efficiency should not be viewed as “saving on taxes” in any given year, but rather a long-term vision of paying as little as legally possible over your lifetime.

Now, I know there’s always an outlier who would argue they’d like to pay higher taxes, we’ll let them exist in their own world for now. Most people would like to pay LESS taxes!

Deferring vs. Saving: Not the Same Thing

The term “saved on taxes” is a bit abused and overused.

Many folks say and believe they have “saved” on taxes when they contribute to a 401(k) or Traditional IRA. Many CPAs and tax professionals, along with many financial advisors, will proudly tell you the value they provided by helping you “save” on taxes.

Ready for this?

When you contribute to a 401(k) or Traditional IRA, we don’t actually know if you saved on taxes. The only thing we can say with certainty is that you deferred your taxes.

That is a very big difference.

So When Do We Convert?

Now that we’ve agreed there is a difference between deferring taxes and saving taxes, let’s explore when to use a Roth account, either through direct contributions or conversions.

A Roth conversion is the action of moving funds from a “deferred” account (such as a 401(k) or Traditional IRA) into a Roth IRA. This creates a tax event. You generate a tax bill and, in essence, stop the deferral of the eventual tax bill that has always been looming over that deferred account.

In the simplest terms:

Defer when your tax rates are higher

Pay (convert) when your tax rates are lower

That alone is the essence of tax efficiency.

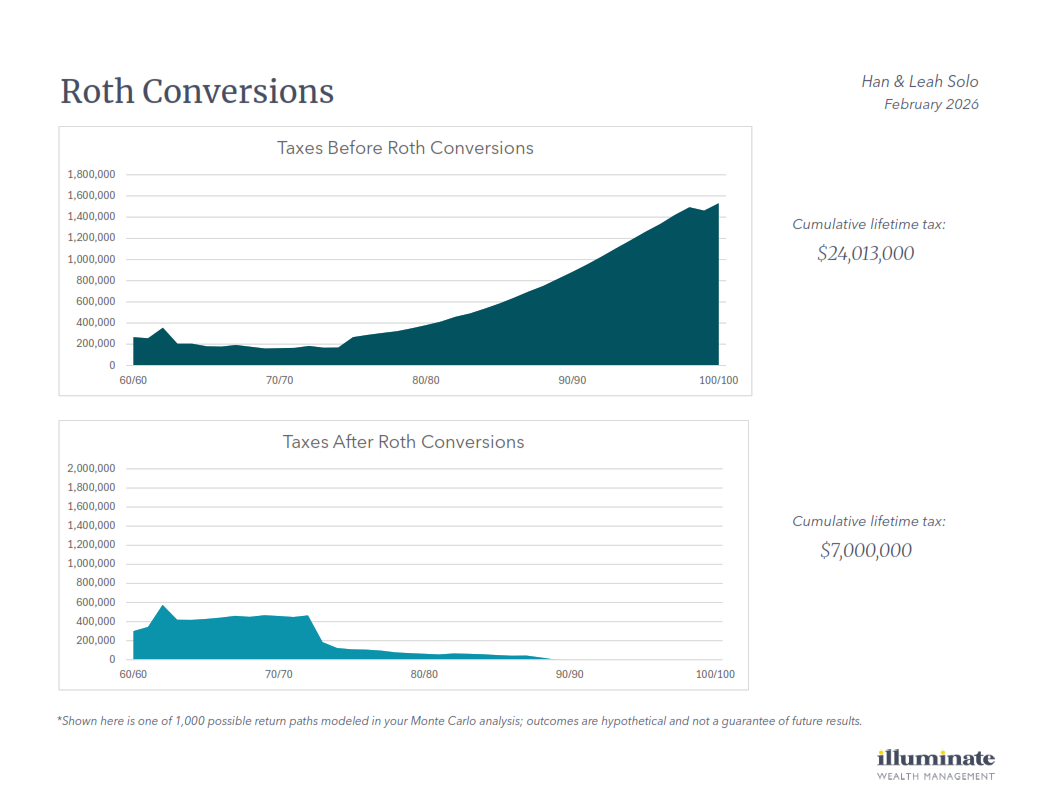

A sample client illustration demonstrating the effect of Roth Conversions on lifetime tax.

Why All the Debate?

Now that we understand what a Roth account is and how a conversion functions, why is there so much debate?

1. The Emotion of Paying Taxes Now

Paying taxes creates a very emotional response in most people. Combine that with the confusion of thinking a deferral is the same as savings, and it’s easy to default to “I’ll just defer.” Facing the fact that the tax will eventually be paid helps reduce that emotional hurdle.

2. Predicting the Future

We know current tax laws and rates. But predicting what tax rates will be in 5 years and especially 20 years is a guessing game. This uncertainty creates a muddy middle where emotion often takes over, and we defer simply because it feels like action.

3. Understanding Your Actual Tax Rate

The tax code is VERY confusing. There are brackets, phase-ins, phase-outs, credits, surtaxes and to add to the complexity, you need to know your tax rate before the clock strikes midnight on December 31st.

Roth conversions are calendar-year sensitive. They cannot be done in April of the following year when your accountant files your return.

This requires income forecasting and, in many cases, software modeling to understand the impact of a conversion.

Wow. It’s no wonder Roth conversions feel mysterious.

If you’d like to discuss how your assets can become more tax-efficient, let’s talk. - Travis