Tax Guide: AGI, Deductions & Capital Gains

It is easy for us Financial Planners to forget how complicated the tax code is for those that don’t spend every day thinking about it. Given income taxes are top of mind right now, with the April 15th deadline rapidly approaching, now is as good of a time as any to address many common tax questions and confusions we’ve seen over the years.

What is the difference between Adjusted Gross Income (AGI) and Taxable Income?

Two of the most impactful yet misunderstood numbers on the tax return are Adjusted Gross Income (AGI) and Taxable Income. AGI is typically the same as total income, adding all the types of income together (with a potential adjustments on Schedule 1). Taxable income, on the other hand, is calculated by taking AGI and subtracting either Itemized or Standard Deduction, giving you a lower number to apply marginal tax rates.

Standard Deduction vs. Itemized Deductions

You have the option to take either a Standard Deduction (flat dollar amount) or an Itemized Deduction to reduce your taxable income. For 2025, the Standard Deduction is $15,750 per taxpayer, meaning you are able to avoid paying tax on that amount.

Itemized deductions include deductions for Medical expenses (over a threshold), charitable donations, mortgage interest and State and Local Taxes (SALT). New for 2025 is that SALT deduction is no longer limited to $10,000, but instead increased to $40,000 for most taxpayers. For many of our clients, this increase in SALT cap now shifts their 2025 deductions from Standard to Itemized, resulting in less tax due.

What is the Enhanced Senior Deduction?

New for tax year 2025, from the One Big Beautiful Bill Act (OBBBA), is the Enhanced Senior Deduction. Taxpayers 65 and older may qualify for an additional deduction of up to $6,000 per taxpayer. This is on top of the Standard or Itemized deduction mentioned above. However, this deduction phases out starting at AGI of $75,000 for Single and $150,000 for Married Filing Jointly (MFJ).

Marginal tax rate vs. Effective tax rate

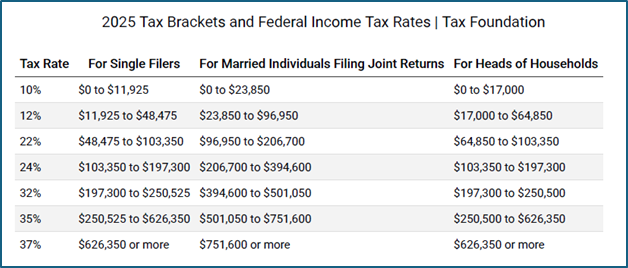

Most of the time, when we talk about tax brackets, we’re talking about “Marginal tax brackets”. This just means how much in Federal tax did the last dollar of ordinary income get taxed. I’m sure you’ve seen this table before (this one from Taxfoundation.org):

In contrast, effective tax rate is calculated by dividing total tax by total taxable income, getting a blended rate. Effective tax rate should always be lower than the marginal tax rate, since the US has a progressive tax system.

Let’s run through a simple example with only wage income to highlight how this works:

Single Taxpayer

Total Wage Income: $125,000

Standard Deduction (2025): $15,750

Taxable Income: $109,250

Marginal tax rate: 24% (using table above)

Total Tax: $19,067 = 10% on $11,925 + 12% on $36,550 ($48,475-$11,925) + 22% on $54,875 ($103,350-$48,475) + 24% on $5,900 ($109,250 - $103,350)

Effective tax rate: 17.45% (=$19,067 / $109,250)

How do capital gains get taxed?

The first consideration for capital gains is short-term vs. long-term treatment. Short-term gains, resulting from sales of securities typically held less than a year, are taxed at your marginal tax bracket (see above). However, Long-term capital gains (LTCG, held more than a year before sale), have their own schedule.

After the ordinary income marginal rates are applied, the rate for LTCG is then applied to realized gains. These rates are 0%, 15% or 20%. In 2025, the 0% bracket is up to $48,350 & MFJ up to $96,700. Then the 15% applies up to $533,400 for Single Filers and $600,050 for MFJ, with 20% applied on LTCG above those thresholds.

Another consideration is Net Investment Income Tax (NIIT), which is an additional tax of 3.8% on investment income for higher earners. In practice, NIIT is why we may talk about an 18.8% or 23.8% LTCG rate, blending the two rates.

Why did I receive an underpayment penalty?

The IRS doesn’t mind giving you a refund, since they held on your money interest-free. However, the IRS (and states) require that you pay in enough in taxes throughout the year, or you will receive an underpayment penalty.

The easiest way to avoid an underpayment penalty is to hit a “safe harbor” amount. This is calculated as the lesser of 90% of your current tax year’s liability or 100% of your prior year's liability (110% for taxpayers with AGI above $150,000). While this seems straightforward, there is some nuance as the IRS intends for you to pay in tax in the same quarter as you earned the income. For instance, if you had a significant taxable income event in January but didn’t pay the requisite tax until November, you would likely still have an underpayment penalty even if you hit the “safe harbor” amount. This is why we look to complete tax projections for our ongoing clients throughout the year, to avoid an unnecessary penalty.

What is a tax extension?

Every taxpayer has the option to extend their tax filing deadline 6 months (to October 15th for individual 1040 tax returns). It is important to note that this extension DOES NOT extend the deadline to pay the applicable tax. When you file the extension, you must estimate your eventual tax liability and pay that amount, even if you wait to file the return until October. There is no penalty to extending, as long as the IRS receives the appropriate tax payment by the normal tax filing date (April 15th for individual 1040).

Have questions about how these tax rules apply to your situation? We’re here to help. Schedule a time with our team to review your tax picture and make sure you’re making the most of every opportunity.