Looking Past the Hype: An Investor’s Guide to IPOs

A wave of potential or widely discussed future high-profile IPOs (e.g., SpaceX, OpenAI, Anthropic, if pursued) are generating significant investor interest. These are companies with strong growth narratives, dominant positions in emerging industries, and a level of visibility that naturally draws investor curiosity. For many clients, the appeal is intuitive: the opportunity to “get in early” on what could become defining companies of the next decade.

But that framing, while compelling, tends to obscure an important point. History suggests IPOs are often underwhelming entry points for investors because of how and when public investors are able to invest in such opportunities. IPOs historically underperformed the broader public market in their early years, even after adjusting for comparable size and style. This is not a short-term anomaly or a function of market cycles, rather a dynamic observed across multiple market periods.

This FAQ outlines what investors should know, including why IPO performance tends to disappoint, how access works, and how these companies ultimately enter portfolios through public markets.

What Investors Should Know

An IPO, or initial public offering, is the process by which a private company offers shares to the public for the first time. It allows the company to raise capital from a broad base of investors and marks the transition from private to publicly traded status. Once listed, shares trade on a stock exchange and are available for purchase by everyday investors.

What Does History Tell Us About IPO Investments?

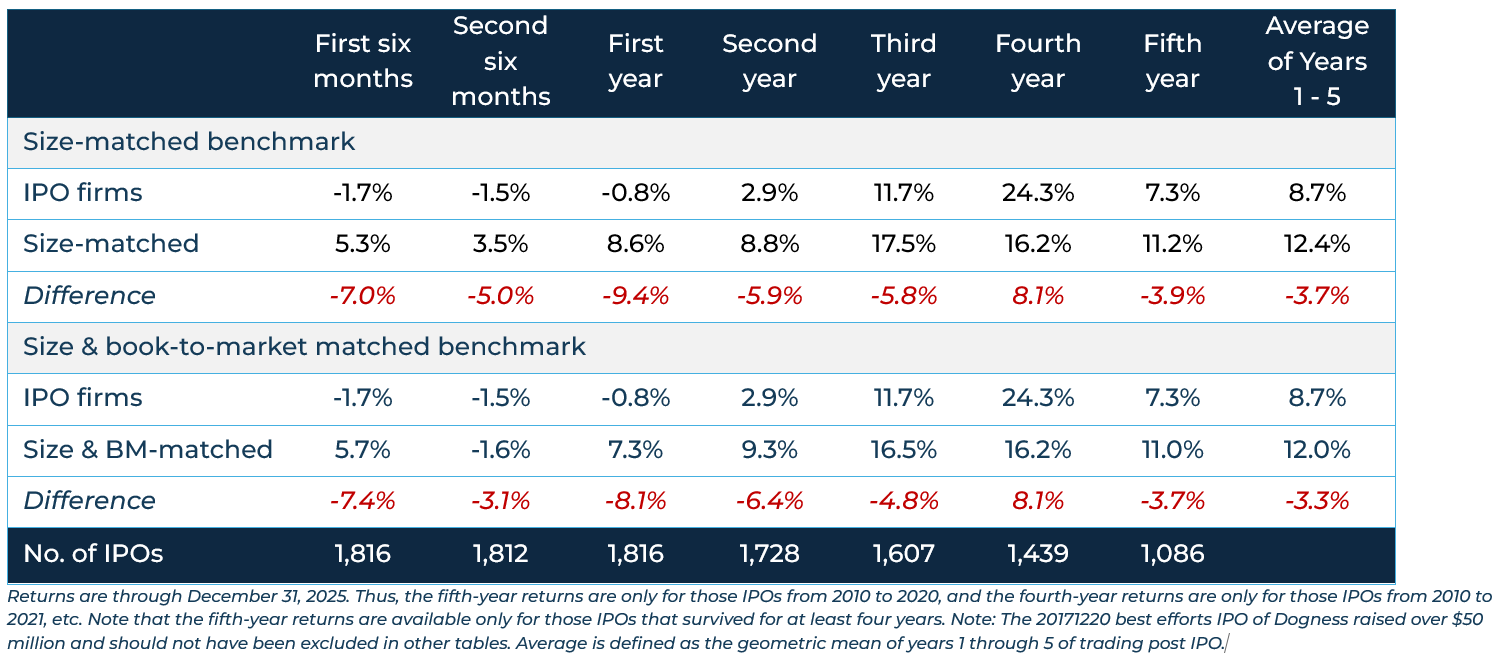

Historically, IPOs underperformed comparable publicly listed companies, a dynamic that is well documented in studies going back to the 1980s and still holds today. Recent data between 2010 and 2024 reflect the same story; in years one and two, IPOs lag benchmarks significantly, by roughly 8 to 9% in year one and 6% in year two, based on size-matched benchmark comparisons in the referenced dataset.

Percentage Returns on IPOs from 2010-2024 During the First Five Years After Issuing

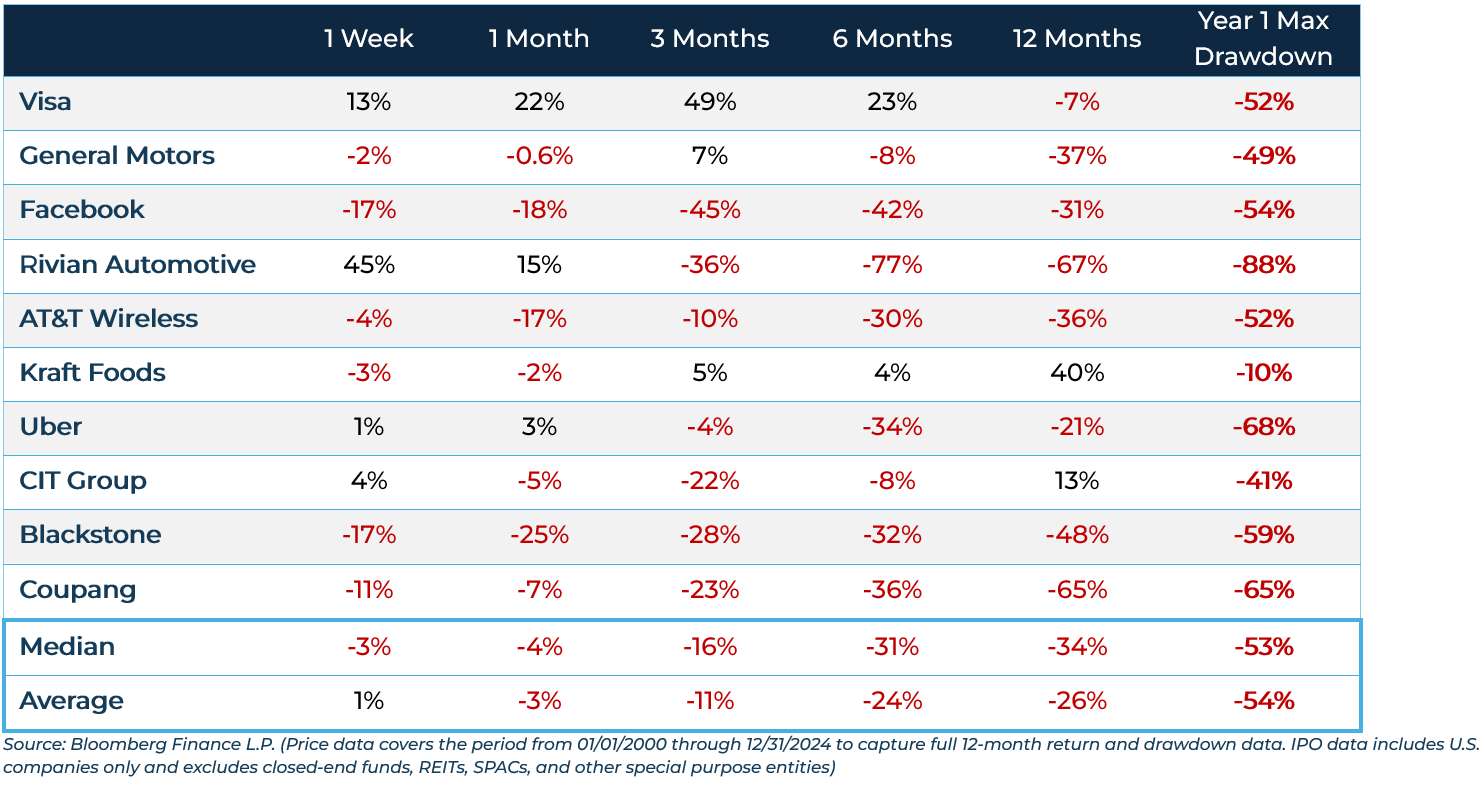

Perhaps more telling than the average return profile is the path those returns take. Even in cases where IPOs ultimately go on to succeed, the early experience for investors is rarely smooth. In the sample of largest U.S. IPOs since 2000 shown here, each experienced a drawdown of at least 10% within its first year of trading, with a median maximum drawdown exceeding 50%. While this is a limited sample, it reinforces how even the largest, high-profile public offerings have historically been accompanied by significant volatility.

Understanding why this happens is an important nuance. IPO pricing often reflects a high degree of optimism, with valuations that already embed strong expectations for growth and execution. At the same time, the supply of publicly available shares is initially limited, with insiders and early investors typically subject to lockup periods. It creates a dynamic where demand outstrips supply in the early days, but where additional shares gradually enter the market over time, often putting pressure on prices. These dueling forces layer into the nuance of the business, limited public market operating history and prevailing macro forces, it becomes clear why early price discovery can be both volatile and uneven.

Forward Returns and Maximum First-Year Drawdowns for Largest U.S. IPOs (2000 – 2024)

The Broad Market Impact From IPOs

How will SpaceX, Anthropic, OpenAI anticipated IPOs impact market indexes?

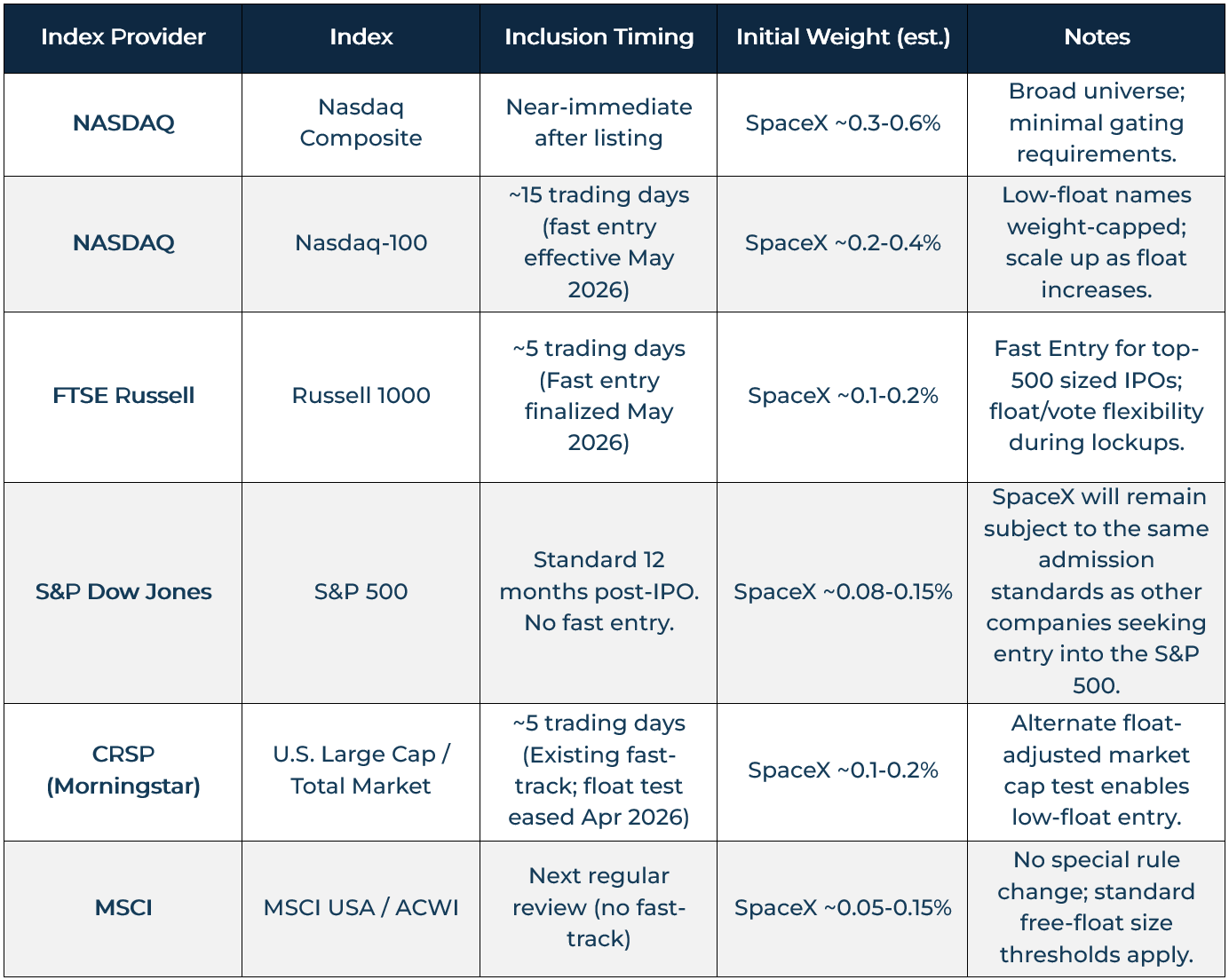

Each index provider has its own rules for when and how newly public companies are added. Historically, most requSired a seasoning period after an IPO before a company becomes eligible. However, the scale of currently proposed listings appears to be prompting providers to revisit long-standing criteria.

There are a few important points to keep in mind:

While pending IPOs (SpaceX, OpenAI, Anthropic, etc.) are expected to set a new highwater mark on valuation, the actual number of shares listed on the exchange (also known as the float) is anticipated to be in the single-digit percentages of total ownership. Many initial holders of the publicly traded shares will also be subject to a 6-month lock-up period.

IPO shares are expected to be included in most major U.S. equity indexes within 5 to 15 days post-IPO, with the exception of the S&P and MSCI indexes (though timing and inclusion are subject to change).

Given the small float initially available, weightings for names are expected to be less than 0.30% each, if not smaller.

Most passive providers (e.g. Vanguard, State Street, Blackrock) are expected to follow the lead of the index providers to include positions within their products and at what weight.

Index Inclusion Timelines by Major Provider

What to Know About Accessing IPOs

How can clients participate in upcoming IPOs such as SpaceX, OpenAI, and Anthropic?

Access depends on the custodian and the specific offering. IPO allocations typically flow through a tiered structure:

• Lead underwriters: Lead underwriters and investment banking partners will often receive the largest segment of allocations.

• Syndicate members: Co-managers and syndicate members receive smaller portions to distribute to their clients.

• Custodial platforms: Custodial platforms may participate if they are included as part of the distribution for a specific deal.

Ability to access will depend on demand and supply. For high-profile IPOs, demand tends to exceed supply therefore allocations are often scaled back leaving investors with meaningfully smaller positions than what they request. For those that do not gain access to shares during the IPO, they can simply purchase the shares after it goes public.

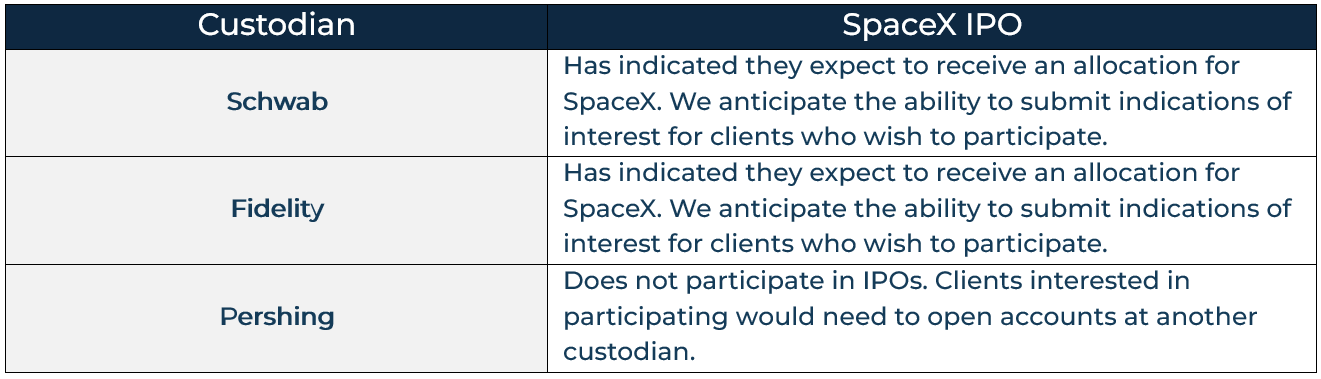

How do Pershing, Schwab, and Fidelity Intend to handle the SpaceX IPO access?

IPO participation may not be appropriate for all investors and should be evaluated on a case-by-case basis within client portfolios. We are actively working with each of our primary custodians to assess what access may be available. Clients will need to provide their written authorization for participation using a prescribed script.

Are There Any Potential Benefits to Buying an IPO?

There are reasons IPOs attract investor attention, but the risks are notable and worth understanding clearly.

Potential benefits:

Early access to companies with strong growth narratives or market leadership in emerging industries

The possibility of price appreciation if the company executes well and the market assigns a higher valuation over time

Key risks:

Early trading is often volatile, and elevated expectations can make the initial risk/reward profile less attractive

Many newly public companies are not yet profitable. For example, the combined SpaceX and xAI entity generated losses of $4.94 billion last year on revenue of $18.67 billion (Source: Morningstar, Securities Filings as of 05/02/2026)

Valuations at IPO often reflect a significant premium relative to peers, implying a high level of embedded optimism that may or may not be justified

Allocation uncertainty is common. Even when retail platforms participate, demand for high-profile IPOs far exceeds supply, and investors typically receive only a fraction of what they request

Conclusion

Bringing this together, the tension around IPO investing is evident. Underlying companies can be attractive, and in many cases, they go on to play an important role in markets, portfolios and the economy. But the IPO itself, meaning simply the moment when shares first become publicly available, is rarely the most favorable point of entry.

As investors, this context creates an opportunity to reframe the conversation. Rather than focusing on access to a specific transaction we should frame it as if, when, and how we choose to gain exposure to the underlying business. In many cases, a measured approach which allows the company to transition into the public markets, for liquidity to improve, and for valuation to adjust, can lead to a less volatile path to ownership. In that sense, IPOs become less about missing an opportunity, and instead about understanding the timing of when an opportunity naturally transitions into a portfolio without creating a negative drag.